Nearly half of Canadians (44%) identify money as their top source of stress, driven by rising costs for housing, groceries, and inflation. For many, this financial strain leads to sleepless nights and anxiety. With nearly one in six Canadians spending more than they earn monthly, it’s clear that managing finances has become a critical challenge.

This is where budgeting proves invaluable. The 50/30/20 rule is one of the most effective strategies for regaining control of your finances. Popularized by Sen. Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan, this method provides a clear framework to balance essential expenses, personal enjoyment, and savings or debt repayment. Whether you want to reduce debt or save more, this guide provides actionable steps to help you take control of your finances.

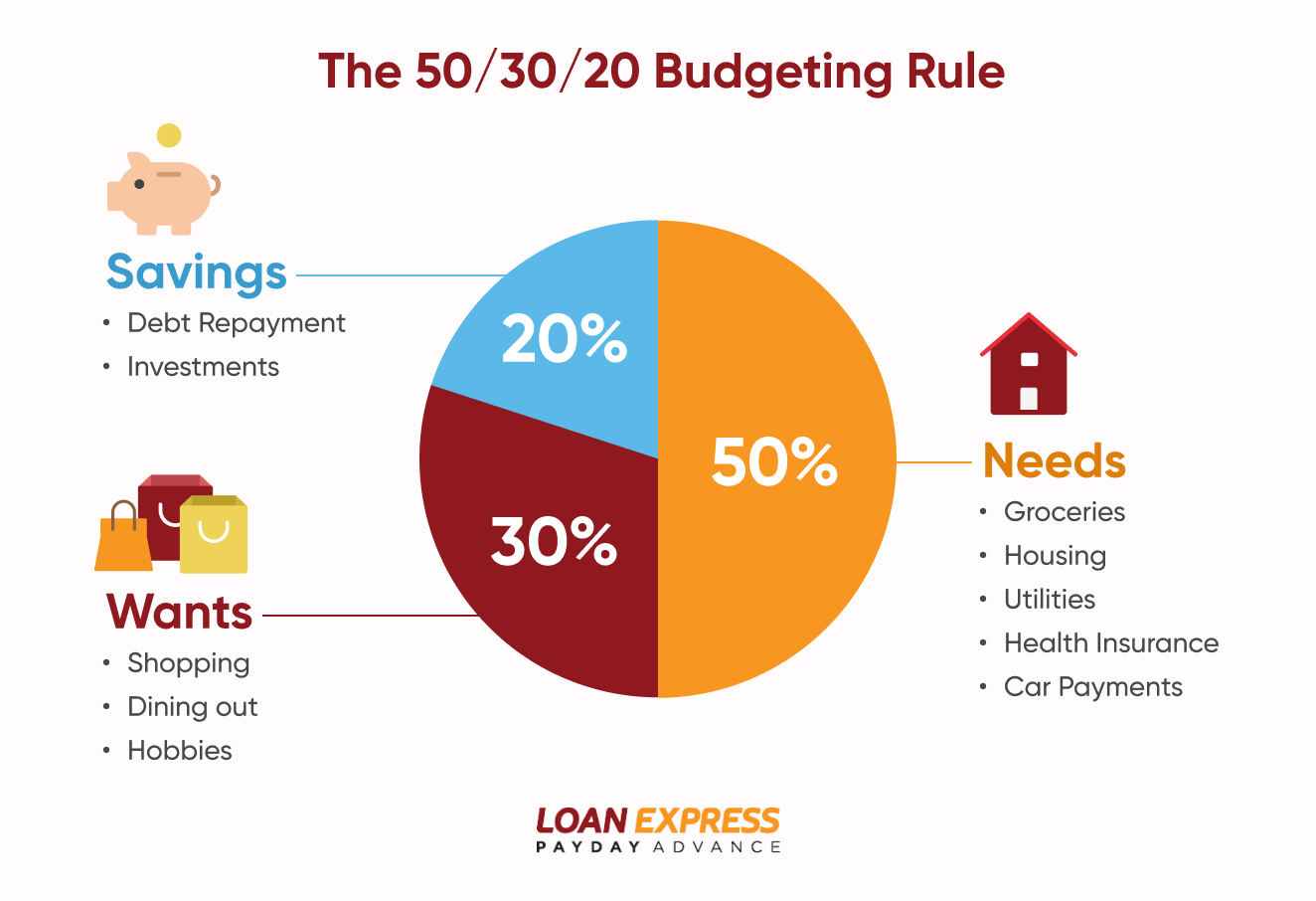

What is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting strategy that organizes after-tax income into three parts. Half of your income (50%) goes toward essential needs such as housing, utilities, groceries, and transportation. The next 30% is allocated for discretionary spending on non-essential items like dining out, hobbies, or entertainment. Finally, 20% is dedicated to savings or debt repayment, helping build an emergency fund or reduce high-interest debt. For example, if your monthly after-tax income is $4,000:

- $2,000 (50%) would cover needs like rent or mortgage payments and groceries.

- $1,200 (30%) could go toward wants such as vacations or subscriptions.

- $800 (20%) would be allocated toward savings or paying down debt.

This structure creates a balance between meeting current obligations and securing future financial well-being, while leaving room for enjoyment.

Why the 50/30/20 Rule Works

The 50/30/20 budgeting method is an effective budgeting method because it simplifies financial management while remaining flexible enough to fit different lifestyles. By focusing on three broad categories instead of tracking dozens of expenses individually, it reduces complexity and makes budgeting easy even for beginners.

Allocating 50% of income to needs ensures that essentials like housing and utilities are prioritized. The 30% for wants allows you to spend money guilt-free. Meanwhile, dedicating 20% to savings or debt repayment helps build long-term financial security by building an emergency fund or reducing high-interest debts.

This is particularly important given that nearly 59% adults feel uncomfortable with their emergency savings. The 50/30/20 rule also encourages mindful spending habits. Tracking expenses reveals areas where discretionary spending may exceed limits, prompting adjustments.

How to Create a 50/30/20 Budget

Creating a monthly budget using the 50/30/20 budget rule involves three clear steps:

Step 1 – Calculate Your After-Tax Income

Start by determining your monthly take-home pay after taxes and deductions. If your employer deducts contributions like retirement savings or health insurance premiums directly from your paycheck, add these amounts back in to calculate your total income base.

Step 2 – Categorize Your Expenses

Organize your spending into three categories:

- Needs (50%): Essential expenses such as rent or mortgage payments, groceries, utilities, insurance premiums, and transportation costs.

- Wants (30%): Non-essential items including dining out, gym memberships, vacations, shopping sprees, or streaming services.

- Savings/Debt Repayment (20%): Contributions toward an emergency fund, retirement accounts like RRSPs or TFSAs in Canada, or paying off credit card balances and other debts.

Step 3 – Adjust as Necessary

Track your spending over one to two months to identify patterns and determine whether adjustments are needed. If needs exceed 50%, consider reducing discretionary spending temporarily. Similarly, if savings goals require more than 20%, adjust allocations accordingly while maintaining balance across all categories.

Common Challenges and How to Overcome Them

Implementing the 50/30/20 budgeting method can present challenges that require proactive solutions:

Challenge 1: Distinguishing Needs from Wants

One common issue is determining what qualifies as a need versus a want. Essential expenses like housing, groceries, and utilities are often straightforward, but grey areas—such as a car upgrade or premium groceries—can complicate decisions. To maintain a healthy financial situation, create a checklist of absolute essentials and discretionary items. Regularly reviewing spending habits can also help identify patterns where wants are mistakenly categorized as needs.

Challenge 2: Sticking to the Plan Consistently

Maintaining discipline over time can be difficult, especially during months with unexpected expenses or social pressures like holidays, which often requires careful planning and budgeting. Automate savings transfers into separate accounts to reduce the temptation to spend money. You can also use budgeting apps with real-time tracking and alerts to monitor spending against set limits. Setting small, achievable milestones could also keep motivation high.

Challenge 3: Managing High-Interest Debt

Debt repayment within the 20% allocation can feel overwhelming when dealing with high-interest loans or credit card balances. Prioritize paying off debts with the highest interest rates first to minimize long-term costs. If debt consumes more than 20%, temporarily adjust discretionary spending to accelerate repayment while maintaining minimum payments on other debts.

Benefits of Adopting the 50/30/20 Rule

The budget 50 30 20 rule offers a range of benefits that make it an effective tool for managing your finances. Here are some of those benefits:

- You gain financial clarity by dividing your income into clear categories, making it easier to track and allocate funds.

- You improve savings consistency, enabling you to build an emergency fund or work toward long-term goals like retirement.

- You reduce financial stress by saving an emergency fund. The Financial Consumer Agency of Canada (FCAC) found that Canadians who actively save report higher financial well-being scores, regardless of income level.

- You tackle debt strategically, dedicating a portion of your income to repayments without compromising other priorities.

- You create a sustainable financial framework that adapts to changes in income or expenses over time.

The 50 20 30 budget equips you with the tools to manage money effectively and at the same time, reduce stress.

Modifying the Rule for Your Financial Needs

Building a strong financial foundation is key to long-term stability and the beauty of the 20/30 50 rule is that it can adapt to fit your financial situation. Whether you’re managing a high income or working with limited resources, it works. For instance, high-income earners often use this flexibility to increase savings or investment contributions, allocating more than 20% toward building wealth.

For those with lower incomes, essential costs like rent and groceries may exceed 50%, requiring a temporary shift in priorities to cover basic needs before focusing on savings. Reducing non-essential expenses like subscriptions or luxury purchases can free up funds. Life goals such as purchasing a home or eliminating high-interest debt can also influence how you apply the 50 20 30 budget.

For example, Gen X stands at a financial crossroads. While many in this generation show strong retirement savings behaviours, they also face challenges like high levels of student debt and caregiving responsibilities. The flexibility of the 50/30/20 rule allows them to balance these competing priorities effectively

Tools to Simplify Budgeting

The 50/30/20 rule becomes easier to manage when you use tools designed to streamline your monthly budget.

- Apps: Apps like Mint automatically categorize expenses into needs, wants, and savings. YNAB (You Need a Budget) provides a zero-based budgeting system that allocates every dollar to specific categories. For those who prefer simplicity, tools like the Budget50 app specifically follow the 50 20 30 budget framework.

- Online calculators: Online calculators such as those from NerdWallet or OmniCalculator, quickly break down after-tax income into percentages without requiring manual calculations.

- Spreadsheets: Spreadsheets offer a customizable option for hands-on users who want full control over their data.

These tools make the 20/30-50 rule accessible and effective for anyone looking to improve financial management. You can also complement them with other apps like grocery budgeting apps to make it all the more easier.

Final Thoughts

The 50/30/20 rule offers an easy yet powerful way to manage finances effectively by dividing after-tax income into needs, wants, and savings categories. It balances immediate necessities with future goals while leaving room for personal enjoyment along the way. Start tracking your expenses today using this method to gain control over your financial future. If unexpected costs arise during this journey toward stability and growth, Loan Express can offer fast loan solutions tailored specifically for your unique needs.

FAQs

Q: What is the 50/30/20 budgeting rule?

A: The 50/30/20 rule divides after-tax income into three parts: 50% for essential needs like housing and groceries; 30% for discretionary spending; and 20% for savings or debt repayment.

Q: Can the 50/30/20 rule work for low-income individuals?

Yes, but adjustments may be necessary. Low-income earners may allocate more than 50% to needs due to higher living costs relative to income. Savings can start smaller, but building financial stability over time remains achievable.

Q: How do I track my expenses for the 50/30/20 rule?

Track your expenses by using budgeting apps, spreadsheets, or even pen and paper. Categorize spending into needs, wants, and savings over a month or two to identify patterns and adjust your budget accordingly.

Q: Can I modify the 50/30/20 rule percentages?

Absolutely. The rule is flexible and can be adjusted to suit personal circumstances. For example, those with high debt or savings goals might allocate more than 20% to savings and reduce discretionary spending.

Q: Is the 50/30/20 rule suitable for paying off debt?

Yes, the rule supports debt repayment within the 20% savings category. You should consider prioritizing high-interest debts first to minimize interest payments.

Disclosure

Total cost of borrowing is $14.00 per $100 lent for a 14-day loan.

Payday Loans are High-Cost Loans.

- BC Licence #50028

- AB Licence #327001

- SK Licence #100056

- MB Licence #39281 (Exp. Oct 18, 2026)

- ON Licence #4716499

- NB Licence #200001546

- NS Licence #202645507

- NL Licence #20-23-LO073-1